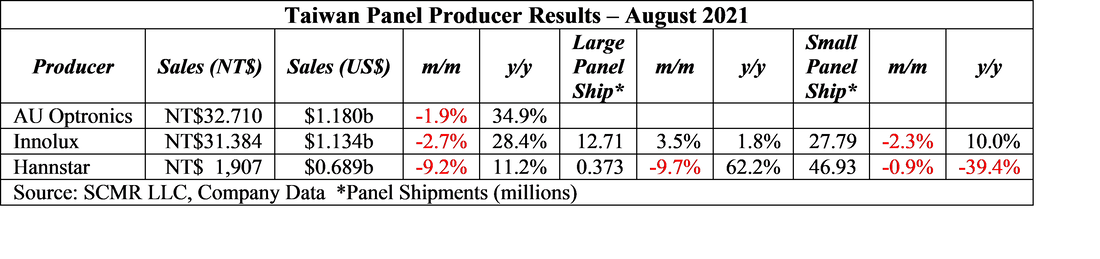

Taiwan Panel Producer Results – October

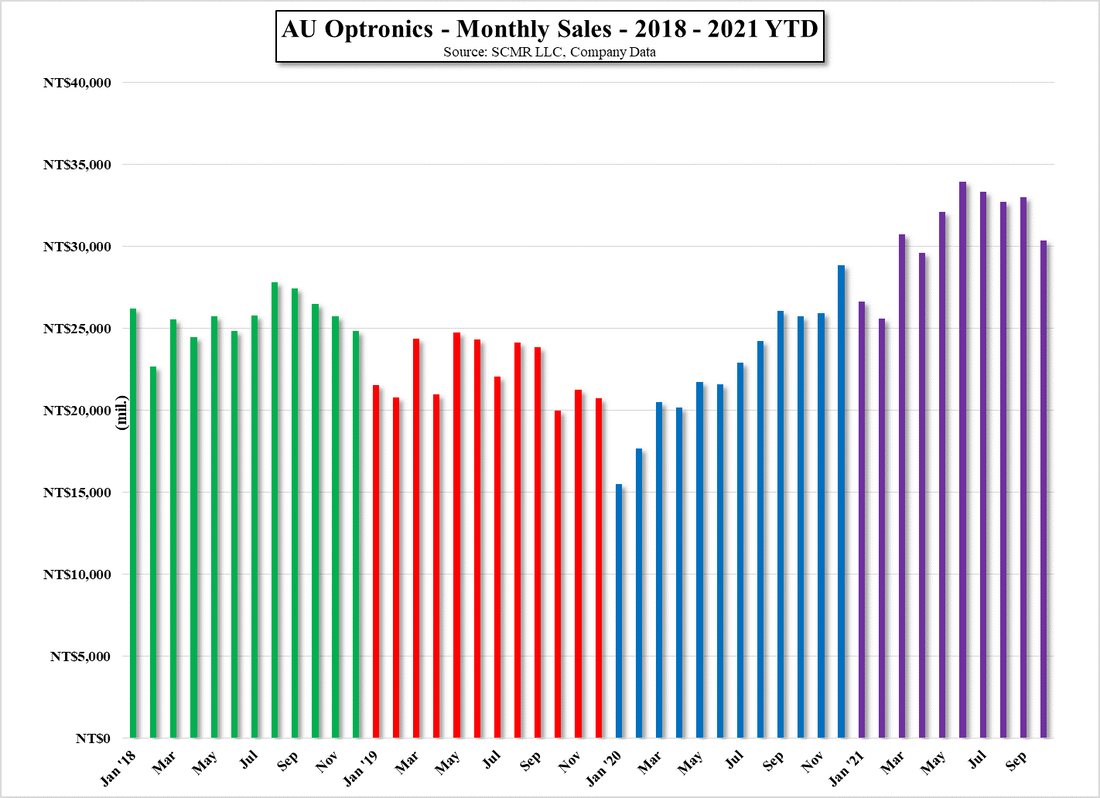

October results were down for all three panel producers in Taiwan, which gives some indication of results for those panel producers that are not seeing an offsetting increase in capacity. While AU Optronics (AUOTY) no longer provides large/small monthly panel data, we expect they saw a reduction in both large and small panel sales in October. AUO still has room to garner positive y/y sales in November, but a strong December last year will make that month a hard comparison, although we expect early 2022 monthly comparisons will return to the positive as sales in January/February of this year were weak. Starting in March however we expect a more difficult time showing positive y/y sales results.

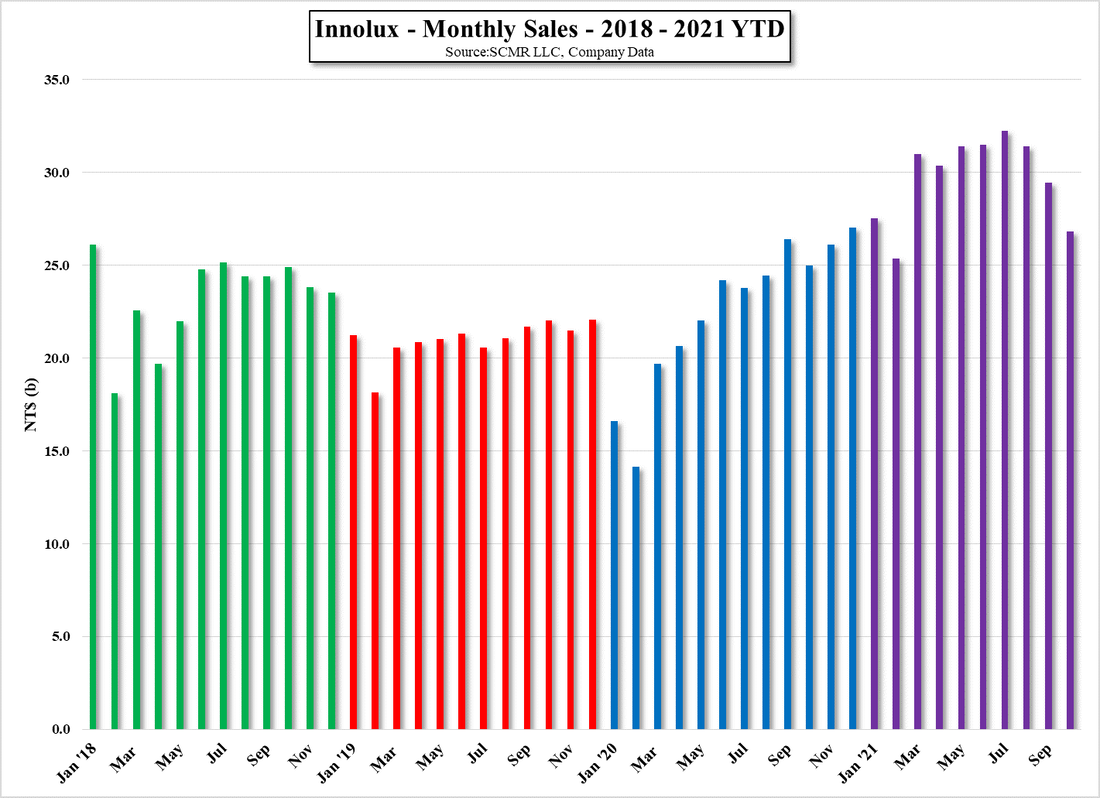

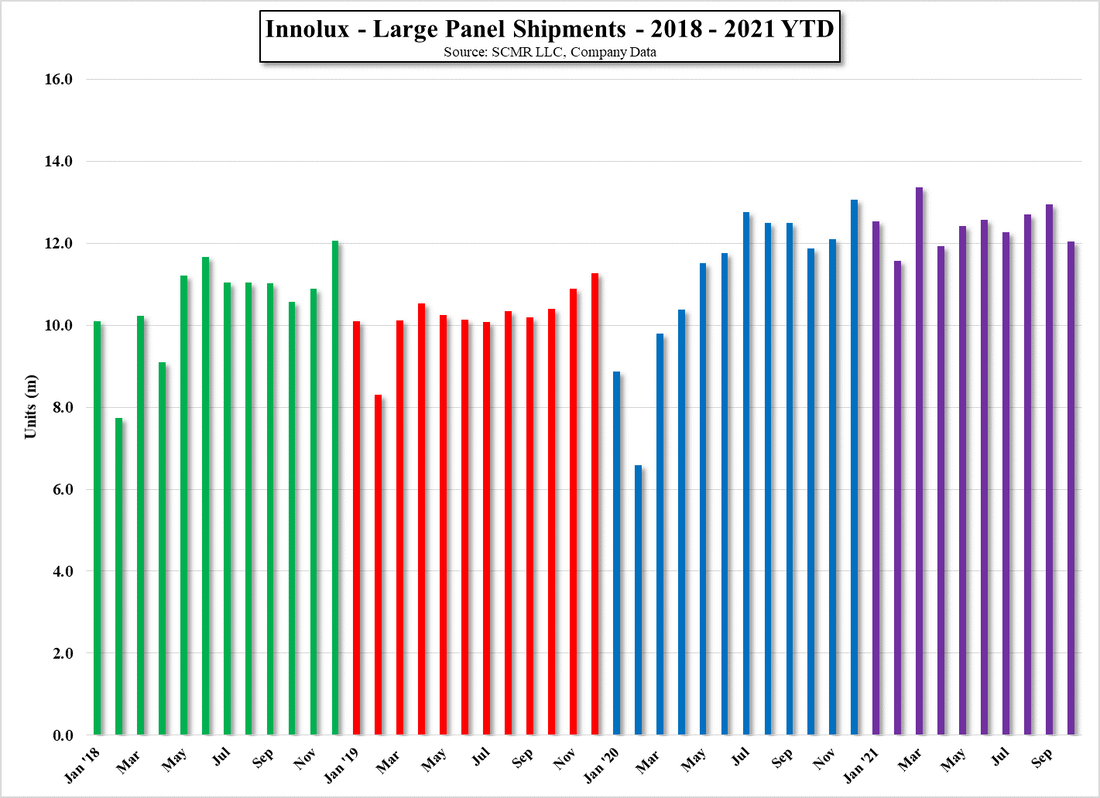

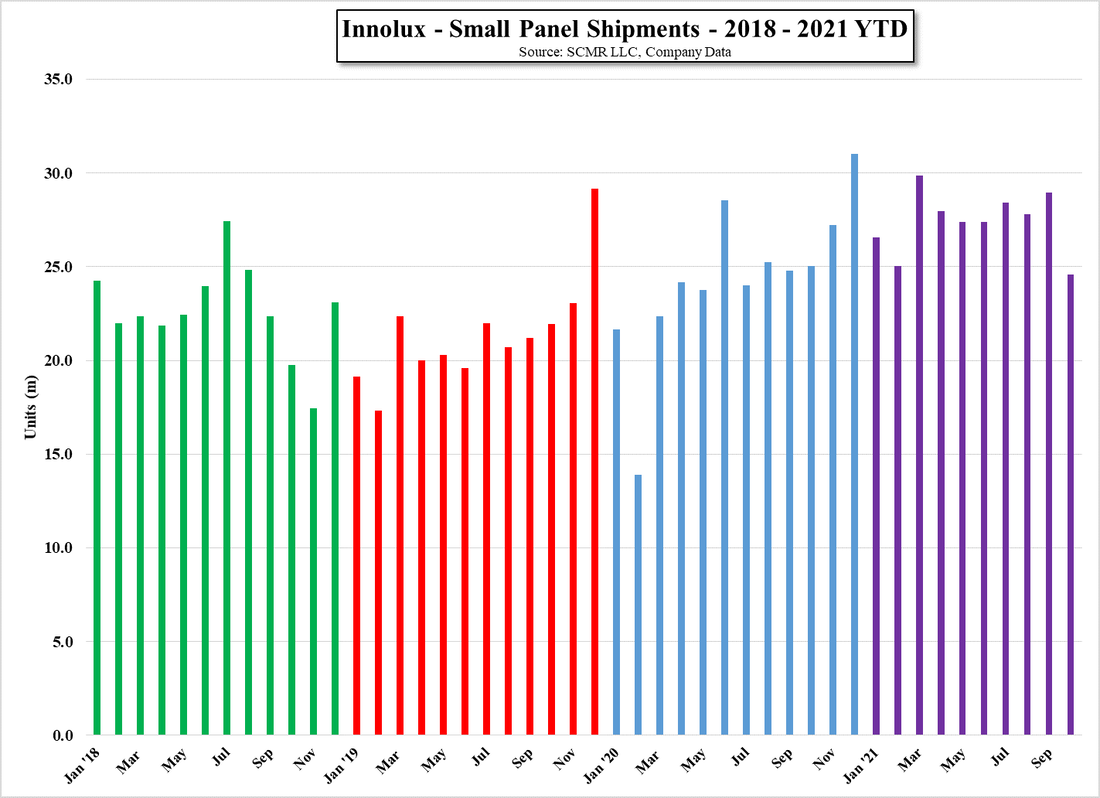

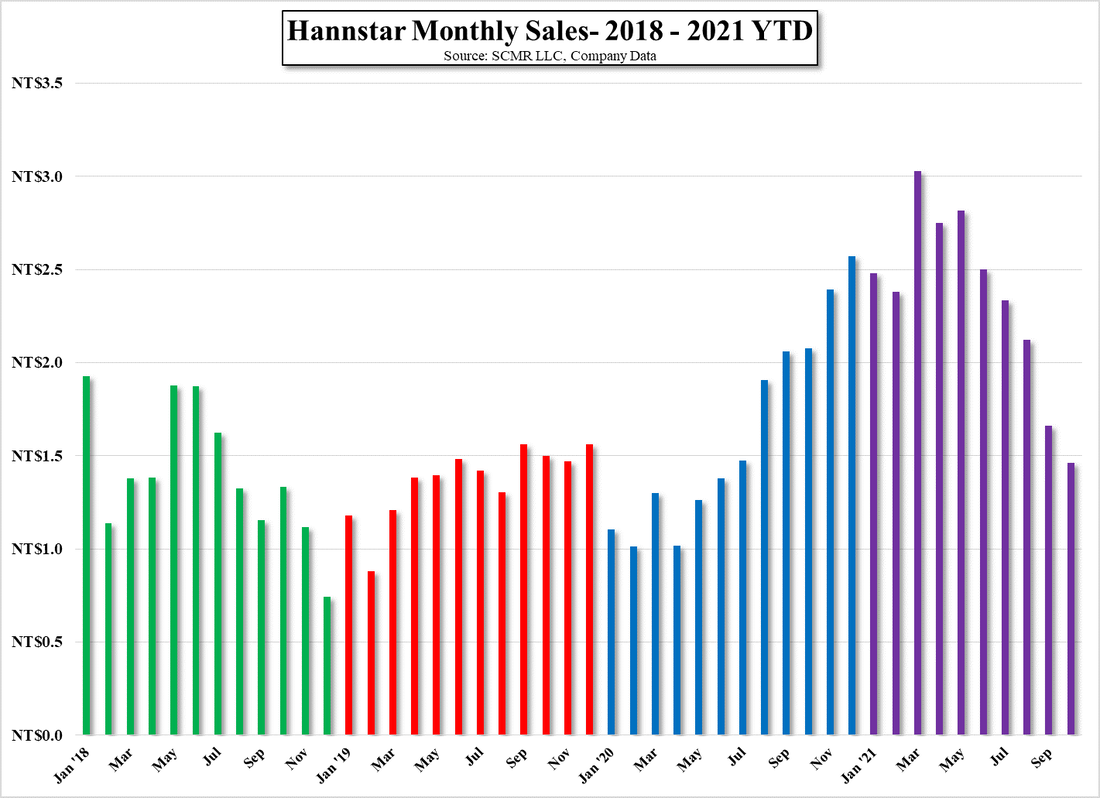

Innolux (3481.TT) has less wiggle room on a y/y sales basis, but relatively consistent large panel shipments have helped to maintain positive y/y monthly sales, however small panel shipments dropped to a yearly low in October, which will impact profitability as small panels are the most profitable on a m2 basis. Hannstar (6116.TT), which is focused on small panel production, saw a continuation of sales declines that began after a peak in small panel production back in March as smartphone demand continues to wane. We would not expect much change until production for the next smartphone cycle resumes in March 2022.

Innolux (3481.TT) has less wiggle room on a y/y sales basis, but relatively consistent large panel shipments have helped to maintain positive y/y monthly sales, however small panel shipments dropped to a yearly low in October, which will impact profitability as small panels are the most profitable on a m2 basis. Hannstar (6116.TT), which is focused on small panel production, saw a continuation of sales declines that began after a peak in small panel production back in March as smartphone demand continues to wane. We would not expect much change until production for the next smartphone cycle resumes in March 2022.

Monthly Sales - 2018 - 2021 YTD - Source: SCMR LLC, Company Data

Innolux - Monthly Sales - 2018 - 2021 YTD - Source: SCMR LLC, Company Data

Innolux - Large Panel Shipments - 2018 - 2021 YTD - Source: SCMR LLC, Company Data

Innolux - Small Panel Shipments - 2018 - 2021 YTD - Source: SCMR LLC, Company Data

Hannstar Monthly Sales - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed